The importance of oil should not be underestimated as an energy source – and a pollutant. Almost every form of transport is dependent on it and its refined products and the present economy would not have been created without it. Most of it is burned by vehicles propelled by the Internal Combustion Engine (ICE), enabling transport of people and goods world-wide. As the number of vehicles increases, so does demand for oil and its derivatives. Little wonder then that oil companies should regard their product as having a long, profitable and relatively secure future.

When it comes to talking about Peak Oil, we often think of it in terms of the point at which the yield from recoverable oil deposits begins to decline. With thawing in the Arctic, new oil deposits are likely to become available, giving the oil industry additional confidence that it will be able to sustain production for at least the next 50 years. Were the industry to think of Peak Oil in terms of the point at which demand for oil begins to decline, then its confidence in being able to sustain production for the next 50 years would seem misplaced for some, if not all kinds of oil.

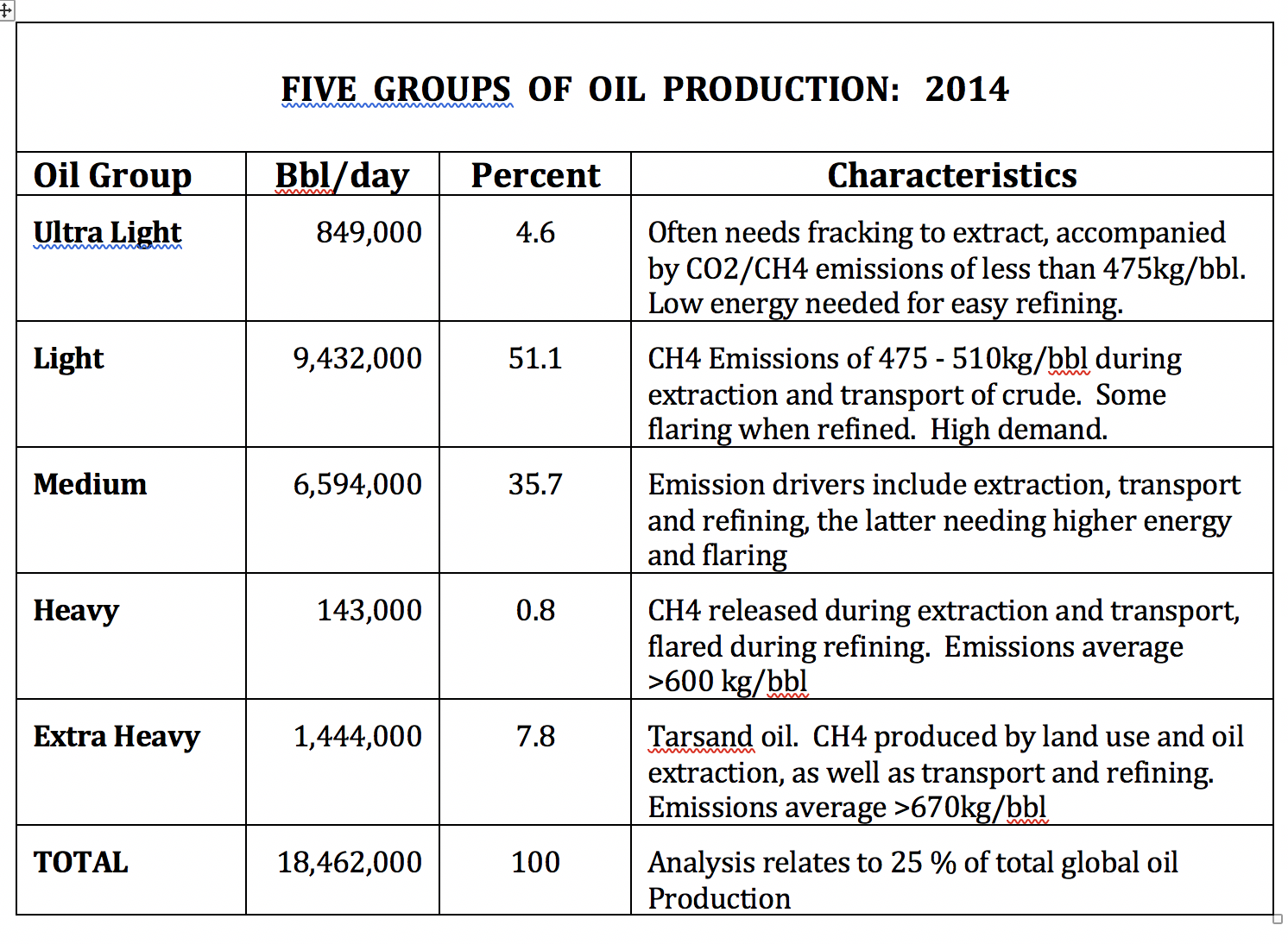

Table 1. Showing difference in characteristics of the 5 groups of oil produced. Source: Data derived from the Carnegie Oil Climate Index covering 25% of global production in 2014.

Table 1 above shows oil is not a uniform product. Some oils are heavier, more difficult to extract and require greater energy to transport and refine. Lighter oils are easily pumped and refined and these oils are the most keenly sought by consumers. Were demand for oil to decline, the first to be affected would be those which are more expensive to extract and refine – the heavier oils – but ultimately all oil production would be affected by a sustained reduction in demand and this would have a significant affect on the economies of oil producing countries, particularly those most dependent on oil revenue.

Why would reduction in demand occur? Improvements have been made to the efficiency with which ICE vehicles burn fuel, thus lowering emissions but this has been off-set my an increase in the number of them in use. At present there are over 1 billion ICE vehicles in use with an additional 80 million vehicles being built each year. There has also been a trend towards production and refining of oils with higher emissions, particularly in North America. The problem with ICE vehicles are thee-fold:

Globally, ICE engines are used in every sector – primary production, all forms of transport and in most other industries. They contribute ~33% of anthropogenic greenhouse gas emissions, making them a significant contributor to global warming, the formation of visible pollution (smog), and posing a danger to public health. This should place downward pressure on use of oil as an energy source but in fact the opposite is true. The present global glut of oil, caused by new drilling technology has enabled higher production, keeping the price of oil below US $60/barrel for the past two years and reducing income earned by oil producing countries.

Despite agreement among OPEC members to limit oil production in order to reduce the oil glut and increase per barrel price, the opposite has occurred because countries most dependent on oil sales as a source of national income (eg. Libya, Ecuador, Iran) have increased oil production in order to maintain national budgets. Petrol and diesel are more abundant and their price has fallen, encouraging their greater use, a trend aided by an increase in the number of road vehicles and likely to continue until 2020 when demand for oil products is expected to reach a maximum. Why should this trend not continue beyond 2020?

For the reasons noted above and on-going advances in battery technology enabling increasingly cost-effective storage of electricity which can replace internal combustion engines with electric motors, particularly in the transport sector. Importantly, these advances are starting to make it cheaper to generate dispatchable electricity from renewable sources, potentially displacing use of all fossil fuels as an energy source.

The number of electric hybrid and electric vehicles (EV’s) on our roads is presently constrained by their price which makes them more expensive than many ICE vehicles, primarily due to the cost of their batteries, the limited range they can be driven on a single charge and, to a lesser extent, the time they take to recharge. However, recent and on-going advances in technology continue to address these issues with the result that the purchase price of EV’s are destined to become highly competitive and, in less than a decade, cheaper than many ICE vehicles.

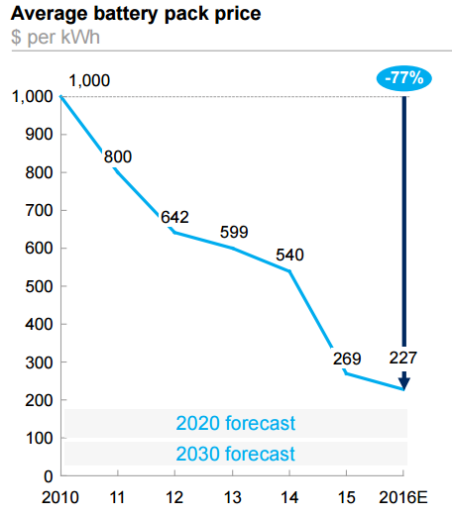

Batteries are the most expensive component in an EV so the price of these vehicles is largely dependent on battery costs falling, on their ability to store electricity rising – as well as on growth in uptake of EV’s by end users. Battery costs have fallen by more than 80% over the last 8 years while their energy density has increased the range of some EV’s from less than 100 km to around 400 km over the same period. These developments are being driven by competitive demand for improved EV’s and the growing need of solar and wind generators for greater storage capacity.

Fig 1. The widely available price for EV battery packs was $227 in 2016 but as noted below, in 2017 the price has declined to well below $200/kWh. Source: Elektrek.

For EV’s to sell at or below the price of ICE vehicles, the cost of batteries must fall to around $100/kWh. Tesla CEO Elon Musk claims that his megafactory (now 1 of many competing megafactories) has been producing EV battery-packs at less than $190/mWh since early 2016.

In 2017 there have been reports of recent EV battery sales at under $140/kWh, while Audi claims that battery packs for its up-coming electric car range will cost it around $114/kWh. It therefore seems possible that over the next 3 years battery capacity will enable most EV’s to travel a minimum of 500 km on a single charge. By 2020, battery prices are likely to have fallen further, possibly to less than $100/kWh.

This will make the purchase price of most EV’s competitive with ICE vehicles, stimulate accelerated uptake of EV’s and result in decline in demand for ICE vehicles and their fuels. Bloomberg suggest a sustained 45% compounding growth rate in uptake of EV’s in the 2020’s is likely.

These changes will be aided by the fact that EV’s are much cheaper to run and by public policy of supportive governments aimed at reducing fuel imports, saving foreign exchange and reducing greenhouse gas emissions. Evidence of this is provided by French and British Government announcements banning sale of ICE vehicles after 2040, a date which could be brought forward as technological advances are realized.

Competition among battery producers – and users – will ensure that the most cost-effective commercial batteries reach the market at the earliest date. Aluminium-air, solid state, even glass based innovations all offer significant improvements over lithium-ion batteries, both in terms of charge density and recharge time, the latter being reduced from hours to minutes and demand for them is particularly high, nowhere more so than in the transport sector.

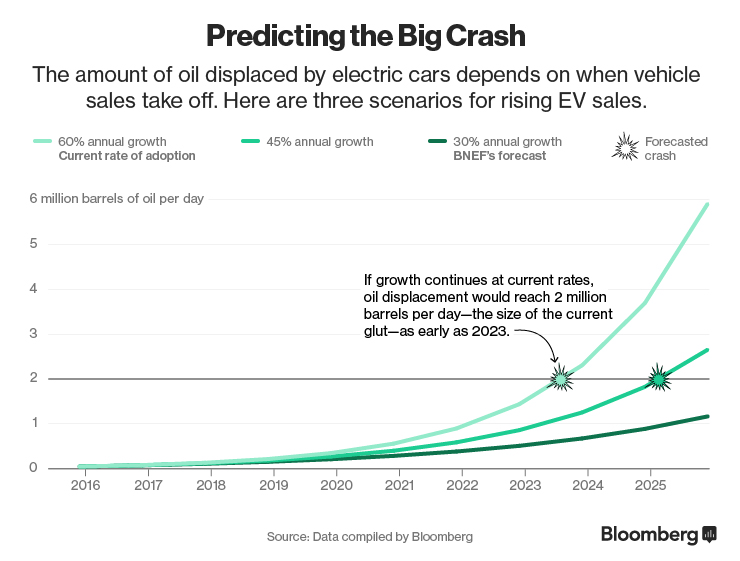

Fig 2. Bloomberg analysts predict that uptake of EV’s will reduce demand for oil by 2 million barrels/day, possibly by 2023 and certainly by 2025. This is sufficient to cause a permanent and increasing reduction in demand for oil, placing downward pressure on its price, making it increasingly unprofitable to extract and refine.

Most major motor vehicle builders now produce plug-in hybrid electric or purely electric vehicles, with Volvo becoming the first manufacturer to announce its intention of ceasing production ICE propelled cars. The trend away from ICE propulsion is very limited at present but will grow as EV battery prices decline and their storage capacity increases during the early 2020’s. The advent of autonomous vehicles could stimulate EV fleet sales since they are more profitable and safer to operate and can provide cheaper, more convenient transport to a population segment now dependent on taxi’s, car hire or public transport.

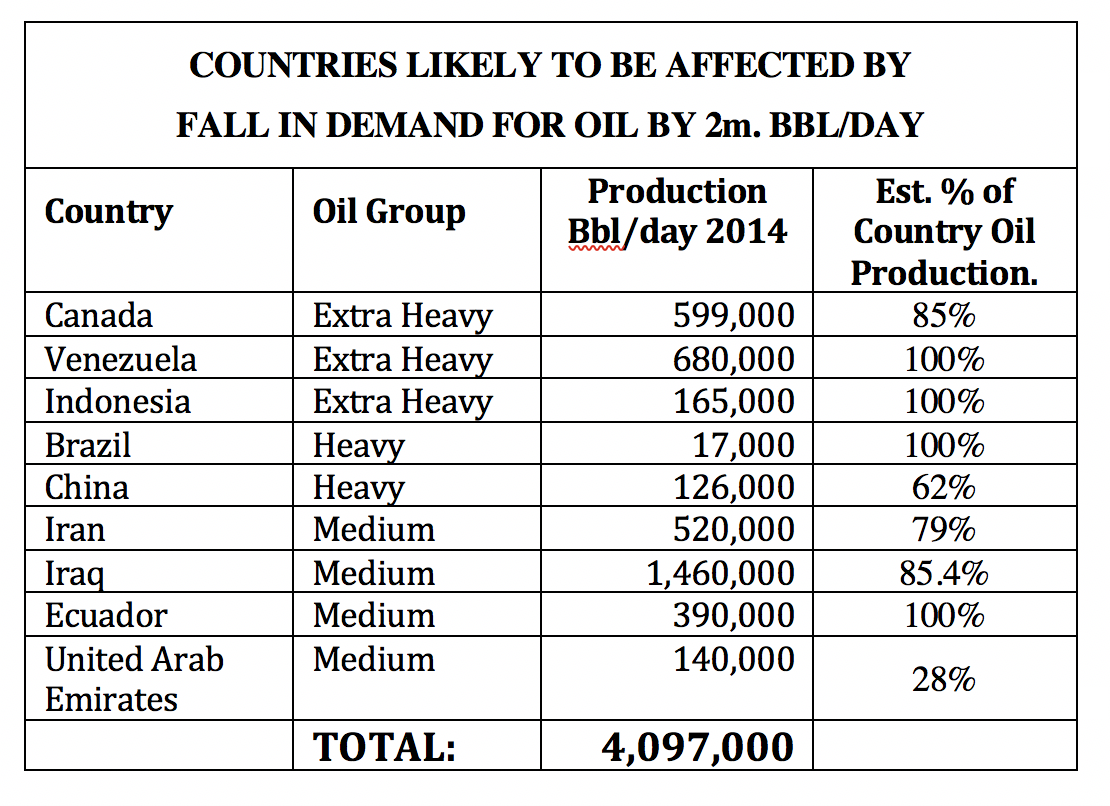

However the most significant impact of EV’s will initially be on those countries producing oil which is the most expensive to extract and refine, particularly those most dependent on oil exports and revenue for public expenditure. Those countries will experience rapid contraction of their oil markets and revenue earned from them. Some producers may, as they are presently doing, seek to off-set a fall in oil price and revenue by increasing production but this will only exacerbate a demand driven oil glut and accelerate price collapse.

Table 2: Countries most likely to be affected by reduction of 2 million bbl/day in demand for oil based on cost of extraction and refining. Source: Data derived from the Carnegie Oil Climate Index.

It is for this reason that some major oil producing countries, notably Saudi Arabia and Iran, are diversifying their economies, reducing their dependence on oil production and its revenue stream.

Ultimately - and more rapidly than many now think - oil production/refining companies will be faced with the need to contract or stop production, significantly reducing the value of their assets and ultimately, seeing them become stranded assets of little value followed by closure. Some countries (eg. China, Brazil) may continue production purely for domestic use. Others (eg Venezuela, Canada, Ecuador) are likely to see collapse of their heavier oil export markets.

Advances in battery technology now being made will have a much wider effect than curbing use of oil for transport. They herald an all pervasive, permanent change from reliance on fossil fuels as our prime source of energy to electricity generated from solar, wind, tidal and geothermal sources, stored for optimal use.

Posted by Riduna on Friday, 18 August, 2017

|

The Skeptical Science website by Skeptical Science is licensed under a Creative Commons Attribution 3.0 Unported License. |