Problems

Australia is the worlds’ largest exporter of coal, selling thermal coal for electricity generation and coking coal for smelting world-wide. In 2017 its export of this commodity was valued at over $40 billion, most of it produced in Queensland and New South Wales. In addition, coal is mined for domestic use with about 42.3 million tonnes,valued at over $4 billion being consumed in 2017, primarily for generating electricity.

Federal and State governments make important financial gains from this through collection of royalties and income tax on coal production and sale. These gains enable governments to provide quality essential services which assist in maintaining a high standard of living for all Australians and sustain rural towns with steady employment provided directly by mining operations and related industries dependent on them.

However, a problem with coal is that its mining involves emission of methane and Australia has 21 coal mines currently in operation. The volume of methane emitted by them is not accurately known nor is it known if those emissions are included in official estimates of national emissions. A more serious problem is that when burnt, coal produces carbon dioxide (CO2) and is estimated to be responsible for 30% of all CO2 emissions in Australia – and world wide.

As such, coal production and combustion are major contributors to global warming and its effects on climate which in recent years have been marked by increases in the frequency and severity of weather events world-wide. These increases have prompted growing public protests, particularly by younger people and calls for governments to be more active in planning and acting to curb greenhouse gas emissions.

Fig 1. Dead fish floating on the Darling River at Menindee, 2019. Rivers stopped flowing. Over 1,000,000 fish died from hypoxia. Picture: Robert Gregory/AFP.

Fig 2. Livestock losses due to drowning in the 2019 North Queensland floods and subsequent starvation estimated at 500,000 head. Source: The Guardian.

In Australia, damage caused by severe weather events in 2019 has included prolonged drought and fires, floods and heatwaves producing record high temperatures and extending summer temperatures by 5-6 weeks. Their effect has seen massive loss of habitat and wildlife, huge losses of property and livestock which will take 3-5 years to replace – provided there is no repeat of the destructive events causing them. Recovery from the damage caused by 2018 events is estimated to cost $18 billion.

Major users of coal to generate energy, particularly China and India have found that, apart from greenhouse gas emissions, coal combustion results in high levels of particulates which cause visible air pollution (smog) endangering public health and contributing to premature deaths. Another by-product of burning coal in power stations is the generation of massive volumes of ash, often stored in areas where it can leach into waterways making them unpotable and contaminating fish, making their consumption dangerous to health.

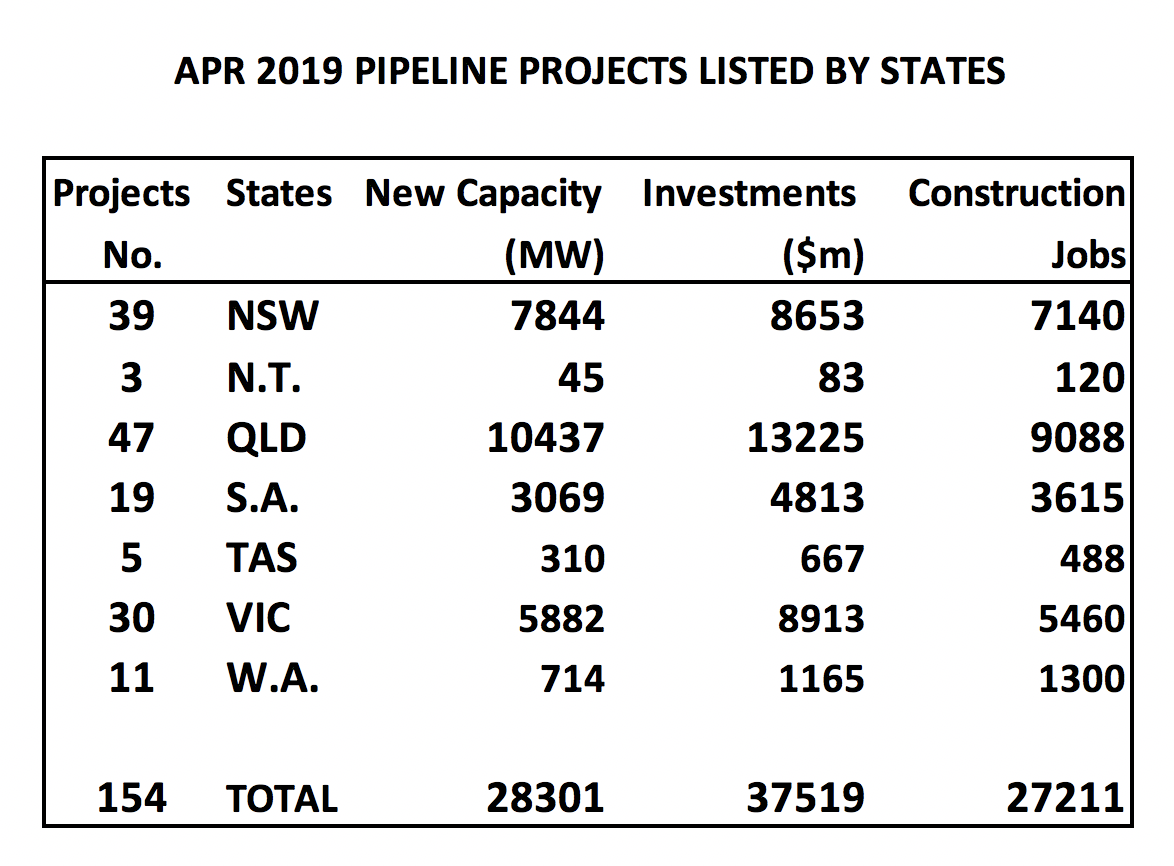

Fig 3. Renewable energy projects approved to be built and commissioned in Australia over the next 3 years. Over 50 projects are likely to complete in 2019. Note: This Table excludes major proposals such as Snowy 2.0 (energy storage) and the Pilbara Power Hub (9 GW for export) which are not yet ‘shovel ready’. Source: Authors research and Clean Energy Council data.

Demand for Australian coal for domestic use is declining as the nation transits to renewable energy. As shown above, $37.5 billion is expected to be invested in electricity storage, solar farms and wind turbines over the next 3-5 years. Australia is not the only country moving away from coal to renewable energy sources. Many countries are replacing coal with gas because it is cheaper. It also has lower greenhouse gas emissions when burnt.

If undertakings by countries subscribing to the Paris Accord are to be met it is inevitable that global coal-fired electricity generation must decline. This will be accompanied by transition to renewable energy sources, primarily wind and solar. China, the worlds’ largest user and second largest importer of coal, has announced that its import and use of seaborne coal will fall - a trend likely to continue in coming years. Countries, such as The Netherlands, Italy, Germany and others could stop using imported coal by 2030 or sooner, resulting in continuous decline in global demand from 2020 until its use ceases completely by 2050.

Given this scenario, it came as no surprise that in 2017/18 Rio Tinto sold all of its coal mining assets in Australia or that more recently, Australia’s largest coal mine operator, Glencore, should decide to cap its global coal productionat present levels. That decision was taken partly in response to concerns over the effects of burning coal on the environment and achieving Paris Accord targets. What did come as a surprise was the New South Wales Land and Environment Court decision to refuse an application to develop a new coal mine on the grounds that it would contribute to climate change.

These developments have thoroughly alarmed right-wing, climate science denying members of Australia’s Coalition Government, particularly those from the National Party. They have been vocal in calling for a new coal-fired power station to be built in Queensland to ensure supply of cheaper electricity 24/7, to increase domestic use of coal and protect coal mining jobs. The implication being that massive job losses and blackouts will occur damaging the economy unless such action is taken.

The Prime Minister and Liberal Party Leader who faces a General Election in May 2019, has ruled out the proposal, correctly noting that the Queensland Labor Government would never give approval for a new coal-fired power station. To placate pro-coal, right wing members of his own Party, government invited expressions of interest in receiving public subsidies for the cost of continuously supplied electricity.

The need to offer public subsidies arises from the fact that banks and other lending institutions in Australia will not lend for such ventures or for new coal mining proposals. The commercial risk is deemed too high since energy from renewable sources is now generated and stored more cheaply than it can be from fossil fuels.

Subsidising the price at which future generation is sold could overcome this problem for proponents but it raises a moral – and political - question: Should Government use public money to subsidise increased emission of greenhouse gasses, particularly at a time when severity of weather events is increasing, making it an important issue for the electorate just prior to a General Election being held? The Coalition Government proposes doing so.

Demand

What then is the future for Australian coal? At best, bleak. As weather events increase in frequency, severity and destructiveness – and they will – calls for action to reverse this trend will increase in the form of pressure for governments of major coal burning countries to reduce the use of fossil fuels. If such action is not taken promptly, particularly by major coal producing and using countries, catastrophic weather events will become annual events, likely to force mass movement of people searching for the essentials of life.

This will place increasing pressure on major coal-using countries to speed-up their transition, away from coal use to cheaper forms of energy generation which do not emit greenhouse gasses. It will also place pressure on governments of major exporting countries as well as mine owners and operators to plan for retraining of displaced workers and find alternate sources of public revenue.

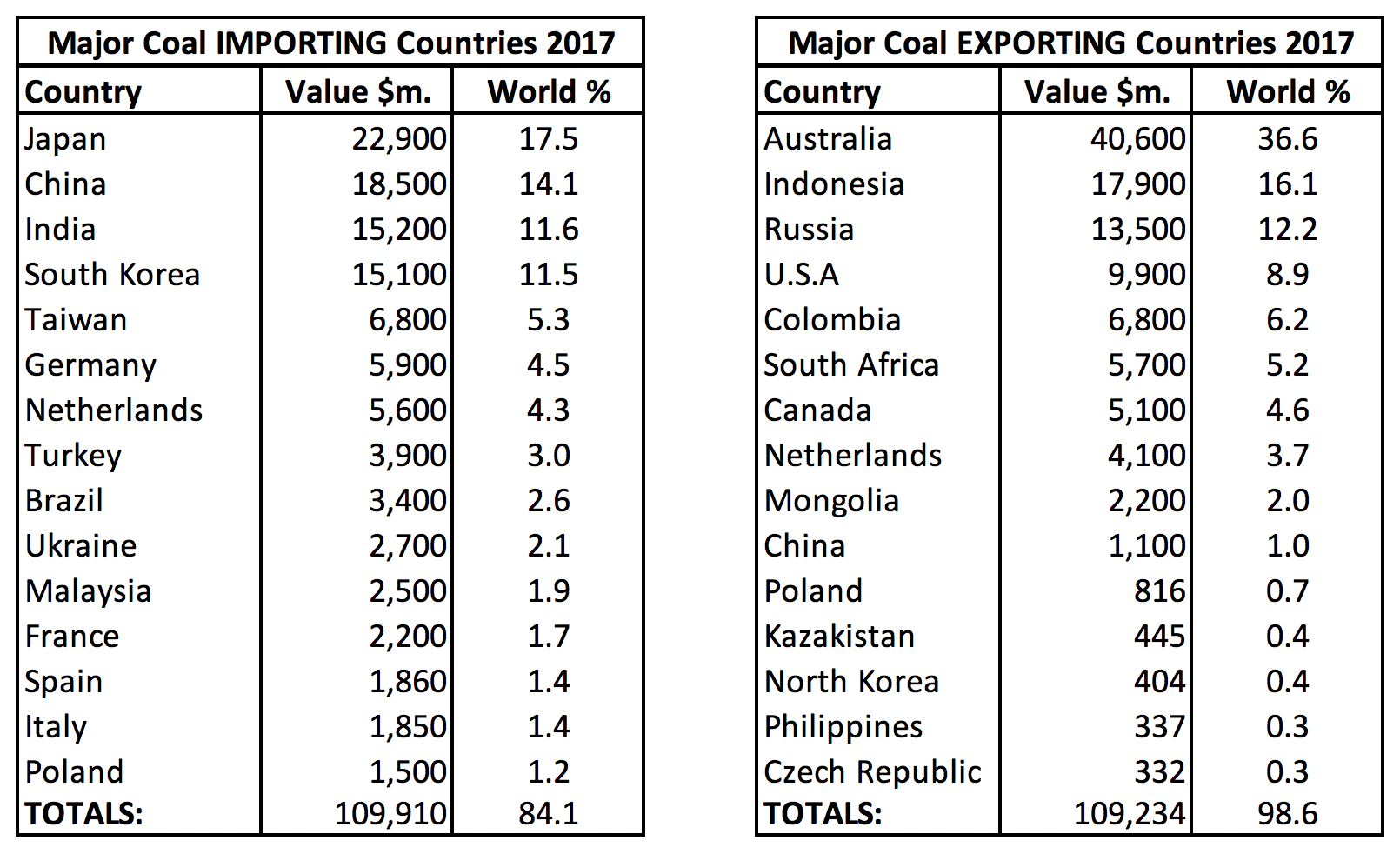

Fig 4. Tables listing the 15 leading countries importing and exporting coal in 2017. Note that some countries (eg. Netherlands) export much of their coal imports. Values in US$. Source for Import data. Source for Export data.

As shown above, the top 15 coal importers account for 84% of global coal imports while the top 15 exporters account for 98.6% of all such trade. It is the exporters who will be the hardest hit by any contraction in demand for coal – and Australia is at the top of that list.

Governments are faced with the task of preparing coal mining communities for contraction of coal mining in Australia with the least cost-efficient mines likely to be the first to close in the 2020's. The task of New South Wales and Queensland Governments, is to ascertain from mine operators the likely operating life of their assets and to approve their plans for environmental rehabilitation. Based on this knowledge, plans to sustain mining communities with other forms of development can be prioritised and developed.

Some politicians, particularly from the National Party, would have us believe that growth of coal use in Australia and overseas is a pressing necessity in order to protect mining communities from sudden mass unemployment, ensure continuity of electricity 24/7 and avoid closure of major industries in central Queensland. This as a ploy to differentiate the National Party from its coalition partner, the Liberal Party as a General Election date gets closer.

The rate at which Australian coal sales diminish will depend on the rate at which the largest importers are able to transition from using fossil-fuels to generate energy to cheaper renewable sources. It is very much in interest of major coal importing countries that they make this transition as rapidly as possible if the goods they produce are to remain competitive with goods made in countries which are moving rapidly towards using the cheapest electricity, that generated by solar, wind, hydro and other renewable sources. This move also conserves foreign exchange reserves now used to pay for coal imports, enabling their use for other purposes.

Major coal importers of Australian coal are moving away from fossil fuels to generate electricity. China and India, two of the larger importers, have indicated their intention of reducing seaborne coal imports over the next decade, while The Netherlands and Germany are likely to phase out use of imported coal by 2030.

On the other hand, ambivalent policy and lack of clear data trends from Japan and South Korea suggest continued imports at around present levels. Between them, they purchase 50% of Australian coal exports. However, pressure from the international community and the need to reduce the cost of electricity in order to remain competitive, could result in them shifting from coal to cleaner, cheaper electricity generation.

Australia is among a growing number of countries moving away from coal to cheaper renewable electricity. As shown by Fig 3, it expects to increase renewable generating capacity by at least 20 Gigawatts (GW) by 2022 and, at the same time, build energy storage sufficient to ensure continuity of electricity supply 24/7. It is likely that a further 20 GW of new capacity will be commissioned by 2026 to cope with economic growth and uptake of electric vehicles.

This could result in closure of all but 5 of the countries remaining 21 coal fired power stations, possibly by 2030, certainly before 2040 with loss of 70% of the domestic market and around $3 billion to Australian coal producers. By 2050, probably sooner, the domestic market for coal will cease to exist.

Conclusion

Claims by right-wing members of the Coalition Government that Australia is faced with an immediate threat to its coal industry are an exaggeration but there is no doubt that over the next decade, mine closures will occur as a result of declining demand for coal. This could result in the decline of coal mining communities over the next 30 years.

This is likely to be compensated for by creation of new industries such as mining of minerals demanded for storage and transmission of electricity, on shore processing of primary products rather than raw exports and innovations in production, storage, processing and transport of food and other goods.

Without such measures, the Australian economy could be severely damaged, not by on-going contraction and eventual loss of the coal industry but because of an increase in the severity and incidence of extreme weather events brought about by on-going global warming. The latter will affect all countries and cause greater economic losses which will eventually prove enduring because they are too costly to recover from.

Australia alone can not avert global outcomes – only effective action by all countries can achieve that – but the country should put itself in a position where it can join low-emitting countries in calling for and enforcing action on major emitters (see Imports Table/Fig. 4) to rapidly curb their emissions. If this is not achieved, we will all lose – permanently.

Posted by Riduna on Tuesday, 16 April, 2019

|

The Skeptical Science website by Skeptical Science is licensed under a Creative Commons Attribution 3.0 Unported License. |